Big Tech's A.I. Race: A Fundamental Investor's Guide

Fundamental Outlook of AAPL, GOOG, META, and MSFT - Stock Market Update

In this analysis of the technology sector's leading companies—Microsoft, Meta, Alphabet, and Apple—there is a singular, unifying theme: a historic and capital-intensive investment to artificial intelligence.

This transition is the most critical strategic challenge these firms have faced in a decade. It's fundamentally reshaping their financial models, competitive dynamics, and long-term growth prospects. The following analyses will delve into the specifics of how each company is navigating this landscape, detailing their individual investment strategies, early monetization successes, and the unique risks they face. What I've laid out is a look into how each of these titans is attempting to secure its future in an era that will be defined by AI.

Let's do a deep dive on their fundamentals and the main key points from the recent earnings reports.

This is the next series of fundamental updates for the "Magnificent 7" and other stocks featured in the Weekly Compass. The upcoming update will cover TSLA, PLTR, and AMZN.

This publication consistently analyzes the following securities to provide a broad market perspective and empower your trading decisions:

Indices & Futures: SPX, NDX, DJI, IWM, ES=F, NQ=F

ETFs: SPY, QQQ, SMH, TLT, GLD, SLV, DIA, SH, PSQ

Major Stocks: AAPL, MSFT, GOOG, AMZN, NVDA, META, TSLA, BRK.B, LLY, UNH, AVGO, COST, PFE, PLTR, NFLX

Crypto & Related: Bitcoin, ETH, IBIT, MSTR

Leveraged ETFs: TQQQ, SQQQ, UDOW, SDOW, UPRO, SPXS, URTY, SRTY

Subscribe now, and unlock all the educational content, the support and resistance levels for all of them every week, and the Weekly Compass with charts and price targets.

Let’s begin with the context and we will continue with the charts in today’s market update.

Microsoft has evolved from a PC-focused software company into a diversified "cloud-first" technology leader. Its primary growth driver is the Intelligent Cloud segment, powered by its Azure platform, which is the second-largest public cloud provider in the world.

Alongside its cloud business, Microsoft operates two other core segments: Productivity and Business Processes, which includes Office 365, and More Personal Computing, which covers its Windows operating system, Xbox consoles, and Surface devices.

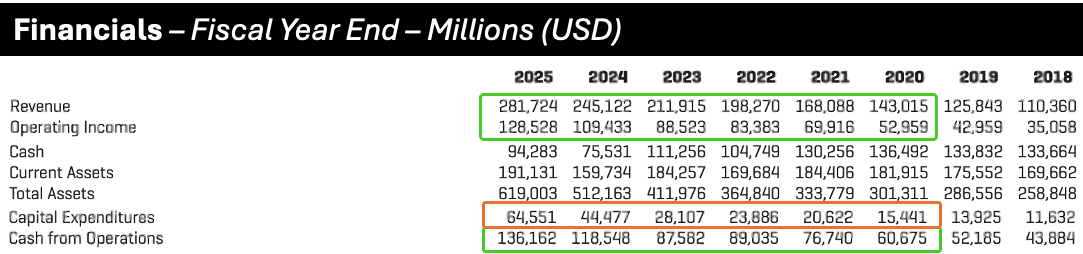

Microsoft Corporation continues executing its strategy centered on Cloud and Artificial Intelligence, delivering strong quarterly results that demonstrate momentum across key business segments.

Key Performance Drivers

Azure and Microsoft's expanding AI portfolio serve as primary growth catalysts. The cloud division reported 39% growth in constant currency during the most recent quarter, exceeding consensus forecasts. This performance is supported by large enterprise cloud migrations and enhanced capacity from new platform deployments.

The company shows progress in monetizing its AI investments, with the Office division demonstrating accelerating Average Selling Price (ASP) attributed to M365 Copilot adoption. This supports the potential for AI applications to drive sustained growth. Microsoft's AI strategy encompasses infrastructure services on Azure—hosting over 1,800 AI models—through application-layer Copilots, enhanced by its strategic OpenAI partnership.

Exceptional Financial Performance

Microsoft demonstrates remarkable financial discipline with operating income growing 23%, on 18% revenue growth, expanding operating margins to an impressive 44.9%. This operational leverage persists despite historic capital expenditures for AI infrastructure buildout, with Q1 capex guided above $30 billion and full-year FY2025 estimates near $64.5 billion. This elevated investment signals strong demand backed by significant backlog, with AI revenue growth now outpacing capex growth—indicating improving ROI on these substantial investments.

Investment Analysis:

AI & Cloud Position: Microsoft benefits from AI trends across both infrastructure (Azure) and applications (Office/Copilot), creating diversified growth opportunities.

Monetization Progress: Accelerating Office ASP and AI revenue outpacing CAPEX provide evidence of developing monetization capabilities and improving investment returns.

Operational Performance: The company demonstrates margin expansion while maintaining record investment levels, with operating margins approaching 45% indicating strong operational control.

Financial Position: Substantial cash from operations (estimated $136 billion in FY25) supports aggressive capex while maintaining balance sheet strength. Long-term debt-to-capitalization ratio is projected to decline to 8.8%.

Risk Considerations

Key risks include slower-than-expected AI adoption relative to current capital spending plans, potentially impacting earnings. Rising compute costs or oversupply could pressure profitability, while tariffs or macroeconomic deterioration might negatively affect gaming and PC segments.