Fed Trapped: Oil, Inflation, Policy Dead End

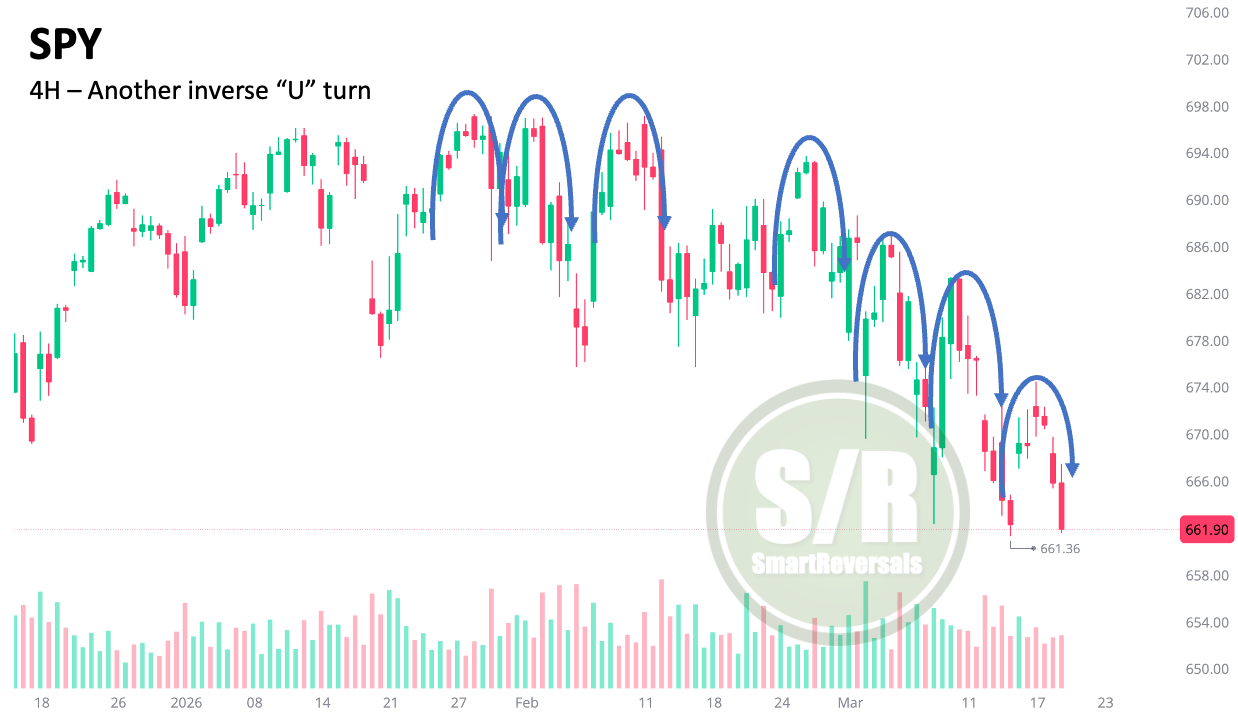

Another S&P 500 Inverse U-Turn in Play

The Federal Reserve held rates steady today at 3.50% – 3.75%, as the market expected. But the real story was not the decision itself, it was what Powell said. When there is a FOMC meeting, you don’t pay attention to the rate decision alone, the Fed Chair words are more important. Similar when you listen to an earnings call, beating expectations is not as important as the guidance.

Powell said the Fed was not making as much progress on inflation as hoped. “The forecast is that we will be making progress on inflation, not as much as we had hoped, but some progress on inflation”

On oil and the Iran War: “Near-term measures of inflation expectations have risen in recent weeks, likely reflecting the substantial rise in oil prices caused by the supply disruptions in the Middle East. In the near term, higher energy prices will push up overall inflation, but it is too soon to know the scope and duration of the potential effects on the economy.”

That said, markets got the answer they feared most: not a hike, not a cut, but a Fed that is stuck.

There are tree forces are converging simultaneously, and each one makes the other harder to resolve.

Oil. Currently consolidating around $96, this is not a demand-driven rally. It is a pure supply shock, the most difficult kind for a central bank to respond to.

Inflation. The Fed revised its 2026 PCE inflation forecast upward to 2.7% from the prior 2.5% projection. The producer price index for February came in at 0.7%, surpassing the consensus of 0.3%. Inflation has now run above the Fed’s 2% target for five consecutive years. The window to “look through” another energy shock is closing.

Growth. Nonfarm payrolls declined by 92,000 in February 2026 and the unemployment rate rose to 4.4%. The Fed’s own projections maintained a 4.4% unemployment rate forecast for year-end, but that assumes stability, not further deterioration.

These three factors create a dilemma that transcends the typical central bank toolkit. While the Federal Reserve can mitigate a banking crisis by flooded the system with liquidity, it cannot manufacture oil. Conversely, aggressive hikes to control inflation could trigger a total economic contraction. With the Strait of Hormuz facing severe disruption, the resulting supply chain shock is already inflating costs and stifling GDP growth

Today, we will examine two key topics: Stagflation and the Current Market Stage. We will compare historical market tops since 1970 with our current 2026 environment and identify the one missing element required for a "full recipe" to confirm that a bear market has begun.

Why that combination? The technical one is related to the current market environment, where inverse U turns in price have been the constant for seven of the last eight weeks for the SPX and the NDX. Two things mentioned in the Weekly Compass last Saturday are happening: 1) The potential Spike in the SPX given extreme oversold conditions (as we saw on Monday), and 2) the inverse U turn revisiting the lows (as it started yesterday and gained momentum today).

On Saturday, I posted the following outlook: SPX is bearish below $6,700.4. I also included specific volatility levels and additional technical indicators to monitor.

This morning, I shared a chart via chat and email suggesting a bearish reversal. This outlook is based on yesterday’s vanishing rally and current bearish conditions, with both the SPY and QQQ trading below their daily levels. Furthermore, the DIA had already broken below its central weekly level.

As noted last Saturday, this is a peculiar market that exhausts both bulls and bears with its rapid spikes and sharp selloffs. Given that the SPX and NDX both touched critical levels today, and a visit to their 200DMA looks imminent, we must assess the potential implications by comparing this price action to previous bear markets.

Upgrade to a paid subscription today to unlock our essential Wednesday analyses, designed for both long-term investors and active traders. This edition alone is worth the monthly subscription, as it provide clear, actionable references for where the market stands today.

Let’s begin.