MAG7 Fundamental Update with Price Targets - Potential Move for the SPX

Price Targets for AAPL, AMZN, MSFT, META, and PLTR as a bonus

As of late March 2025, the "Magnificent Seven" stocks (Apple, Amazon, Alphabet, Meta Platforms, Microsoft, Nvidia, and Tesla) accounted for approximately 32% of the S&P 500's total market capitalization; that figure fluctuates daily, but is a good reference of how important those companies are for the Stock Market and the overall price action in the indices, including also the Nasdaq 100.

For that reason, it’s worth studying their fundamentals in an executive way, focusing on the main takes that can affect their price. I’m also adding Palantir in the fundamental analysis. Last week the fundamental analysis was presented for TSLA, GOOG, and NFLX as a plus. Get access here.

The content for today is:

Fundamental Analysis with Price Targets for:

AAPL, AMZN, MSFT, PLTR, and META

Stock Market Update:

Rare bullish signals and failed cases

Charts: SPX, NDX, NVDA, MSFT, PLTR

Uncertainty Limits Stock Growth

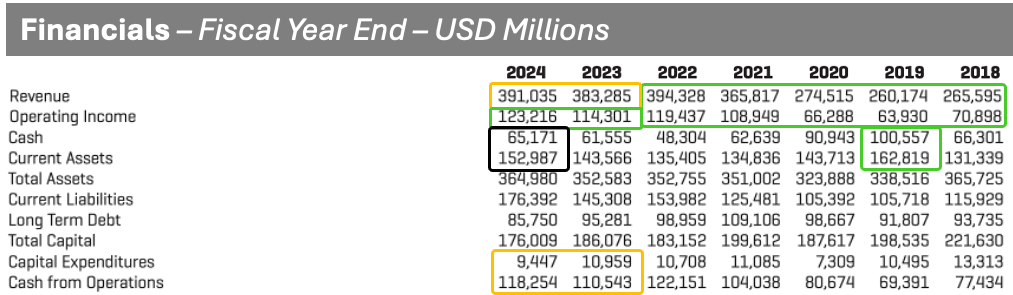

Apple's June quarter sales outlook lacks specific product growth details due to tariff, demand, and legal uncertainties. While the immediate earnings impact is low and long-term tariff navigation is expected to improve, caution is key on near-term profit margins, anticipating further decline after June. Despite this, Apple raised its dividend and buybacks, expressing confidence. The stock shows strong cash flow.

Tariffs: Minimal March Impact, $900M June Cost

March saw limited tariff impact thanks to supply chain management. However, June costs are projected to rise by $900M (net of one-time items) assuming current tariff policies remain. Most US-bound iPhones will be from India, and most iPads, Macs, Watches, and AirPods from Vietnam. The main tariff concern is the 20% rate on Chinese imports, with a total 145% on some China revenues.

Profit Margins Likely to Dip

June's profit margin forecast (46% midpoint) suggests a slight 0.26% year-over-year drop, the first since early 2023. Product profit margins have been declining for five quarters. Long-term margin improvement is expected via tariff offsets and service growth.

The revenues and cash from operations in 2024 neared the highs of 2022, the operating income continued growing, as the cash pile.

Lowered Expectations, Price Target to $226 considering annual level shared in the latest Weekly Compass - Click here.

Solid Start, Second Half Uncertain

Amazon's reported revenue/profit of $155.7bn/$18.4bn beat expectations, thanks to international performance. Unit growth slowed a bit to 8% year-over-year. AWS growth matched forecasts at 17%. Overall, results and the Q2 outlook (slight revenue acceleration) were better than expected, with positive comments on product mix and third-party sellers.

Tariffs Not Yet a Problem, Prepared if They Become One

Management sees limited tariff impact in Q2 profit, citing pre-bought inventory and stable third-party seller prices. April sales were strong. Low-priced essentials are growing fast in the US. Amazon believes its wide selection and strategic buying should help it outperform if retail conditions worsen due to tariffs.

Estimates Going Up on Good Outlook

The Q2 revenue forecast is around $160bn due to stronger retail, while slightly lowering AWS growth. Q2 profit forecast consensus are around to $16.5bn on better AWS margins. The third quarter could see peak tariff uncertainty. Anyway Amazon looks strong with an annual revenue growing constantly and a huge operating income. Capital expenditures are jumping bigly, which is something to watch. $240 is a reasonable annual target.

Upgrade your subscription to paid/premium, click here; get access to all the information in this publication and the links included, continue reading the price targets for MSFT, PLTR, META, and the market update based on today’s Fed meeting, and technical charts for the SPY, NDX, NVDA, MSFT, and PLTR, with a special analysis of historical performance for the SPX.

Strong Azure & AI Lead Microsoft's Earnings Beat

Microsoft's Q3 results and outlook were strong, mainly driven by Azure. Azure's cloud growth hit 35% (constant currency), significantly above the expected 31.5%. This was due to both hardware deliveries and solid cloud migration deals. OpenAI contributed a strong 16 percentage points to Azure's growth (up from 13% in Q2), easing partnership concerns.

Office Growth Remains Solid

The Office business showed good performance with 14-15% constant currency revenue growth, hitting the high end of guidance. Subscriber growth was steady at 7%, though some moderation is expected next quarter. However, strong E3/E5 sales and increasing Copilot adoption support our positive outlook for continued strong growth.

Capex Near Peak, Still Expanding for Future

Q3 capital expenditures were slightly lower than expected (-4% quarter-over-quarter). However, the full-year H2 capex forecast remains the same, and FY26 capex growth is expected to moderate. It’s reasonable to expect around $97bn of capex in FY26 as the peak in the investment for future expansion.

AI Powerhouse in Apps & Cloud; Reiterating Buy

Q3 results suggest that returns on Microsoft's capital expenditures are appearing sooner than anticipated. Azure's core growth is accelerating due to cloud market share gains and AI benefits. Office is also poised for AI-driven growth via Copilot. With accelerating growth, peaking capex, and AI-driven efficiency, free cash flow growth can increase to the high teens in FY27. Considering this context, $475 is a reasonable target for this year. To get access to the chart, click here.