Software: Backbone of the Digital Economy

From Software as a Service to Intelligence as a Service

Every industrial revolution has its toll booths. In the railroad era the toll booths were the trunk lines. In the internet era they were the operating systems. In the era now unfolding, the toll booths are the enterprise software platforms that sit between raw AI capability and the workflows that actually run the modern economy. These are the companies that own the data, the user identities, the audit trails, the sales pipelines, the creative pipelines, the security telemetry, and the service tickets. They are the rails that intelligence has to ride on if it wants to do useful work inside a public company, a federal agency, or a global bank.

During the last months, the software stocks have been impacted in a significant way, but today they’re signaling reversals, the question is: Is that sustainable? Is this an entry point?

Price action is our pillar for technical analysis, and as we always do, understanding the fundamentals behind the chart is essential, today we cover eight of those companies across four roles. Palo Alto Networks (PANW) and CrowdStrike (CRWD) anchor the security stack that every other workflow depends on. ServiceNow (NOW), SAP, and Oracle (ORCL) run the systems of record for workflow, resource planning, and database that touch nearly every Global 2000 balance sheet. Adobe (ADBE) and Salesforce (CRM) own the creative supply chain and the customer relationship on a scale no new entrant can easily replicate. Palantir (PLTR) is the pure play on institutional decision making at the point where data meets operational reality.

Five concepts run through every section that follows:

Data Gravity describes the pull that accumulated customer data exerts on every new workload, making it cheaper to add capability to an existing platform than to migrate away from it.

Switching Inertia describes the operational cost of ripping out a system that thousands of users, integrations, and compliance processes already depend on.

Net Retention Rate measures whether existing customers are spending more over time, which is the cleanest single signal of whether a platform is still the center of gravity for its category.

Remaining Performance Obligations measure contracted but unrecognized revenue, which indicates how much future demand has already been committed by customers in writing.

Platformization, the process of consolidating multiple point products onto a single vendor, is the operating model that turns a collection of tools into a toll booth. Agentic AI is the shift from humans clicking through software to software taking actions on behalf of humans, which raises the stakes on every part of the stack below.

The revenue signal that these moats are holding shows up in the backlog disclosures. Oracle carries $553 billion in Remaining Performance Obligations, up 325% year on year. SAP reports cloud backlog of €77 billion, up 30%. Palo Alto Networks shows RPO of $16.0 billion, up 23%. ServiceNow closed 244 deals above $1 million in a single quarter. Palantir closed a record $4.3 billion in total contract value in Q4 alone. These numbers suggest this is an industry where customers are signing multi-year commitments at an accelerating pace because they have concluded that consolidating spend with a small number of trusted platforms is the safest way to deploy AI without losing control of it.

Net Retention Rate tells the same story from the installed base. Palantir reported a dollar-based net retention rate of 139% in Q4. CrowdStrike holds gross retention around 97% with dollar-based net retention of 115%. These are figures that describe customers who are not only staying but spending materially more each year. That is what Platformization produces when it works. A customer lands with one module, the vendor delivers, the customer adds a second module because the integration is already there, and within three years the vendor is embedded across the enterprise and the relationship has compounded into a consumption curve rather than a license renewal. The final piece of the structural case is the shift to Agentic AI. The incumbent platforms are not defending the old interface. They are building the next one. Salesforce has sold more than 29,000 Agentforce deals and driven the platform to $800 million in ARR in fifteen months. ServiceNow has Now Assist ACV above $600 million and is targeting $1 billion by the end of 2026. Palo Alto Networks is running Prisma AIRS at triple the customer count quarter over quarter. Palantir’s AIP is the reason U.S. commercial revenue grew 137% in Q4. The agents are not an external threat to these platforms. They are the new product line, sold to the same customers, billed through the same contracts, and grounded in the same proprietary data. The toll booth is not being removed. The toll is being collected on a newer road.

Eight Companies - Four Roles - One Stack

Security comes first because every other workflow depends on it. Operations anchors the systems of record that hold the chart of accounts, the service catalog, and the supplier contracts. The creative and front office layer owns the customer relationship and the content pipeline that surrounds it. The intelligence layer is a single name because, at institutional scale, there is only one pure play on decision making at the point where data meets operational reality. What follows is the case on each platform individually, the forward financial profile that anchors it, and the single risk that would most meaningfully change the thesis.

PANW (Palo Alto Networks)

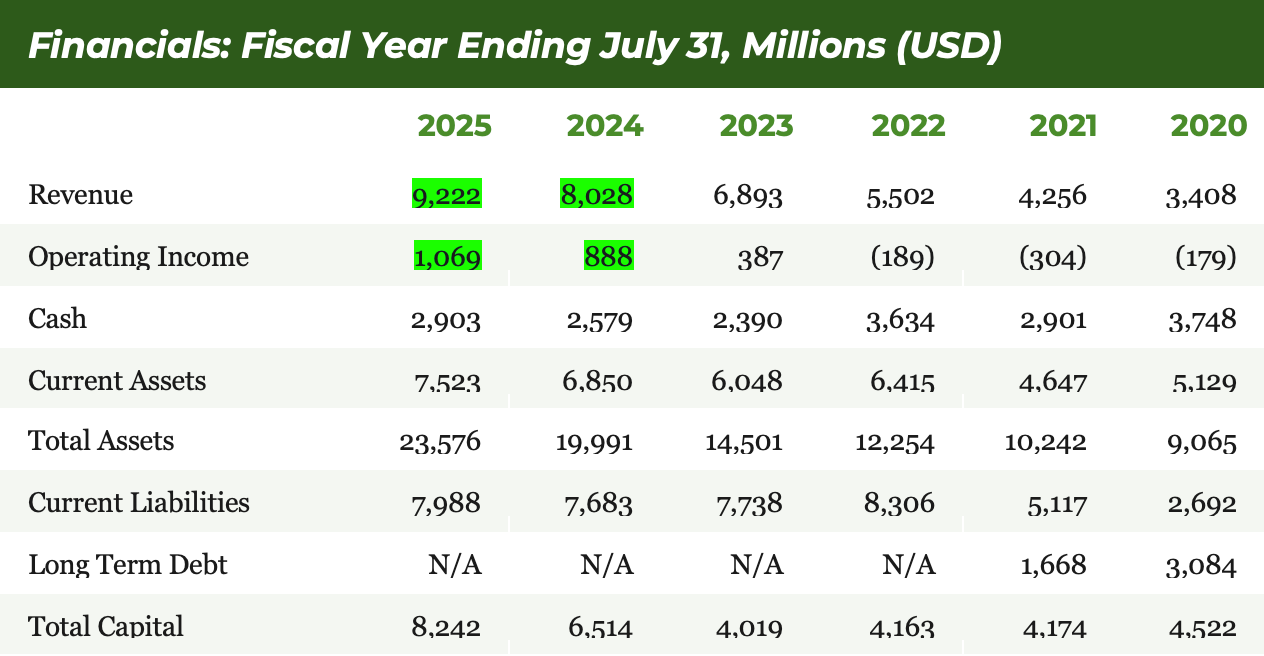

Palo Alto Networks is the broadest cybersecurity platform in the market and the clearest example of Platformization in security. The company serves more than 85,000 customers in 150 countries, including 77 percent of the Global 2000, and has spent the last five years converting itself from a firewall vendor into an end-to-end platform that spans network security, cloud security, and the security operations center. In Q2 FY 2026 that strategy produced Next-Generation Security ARR of $6.33 billion, up 33 percent year over year, and SASE ARR above $1.5 billion growing 40 percent, which makes the company the fastest-growing SASE provider at scale.

The February 2026 close of the $25 billion CyberArk acquisition added a full platform of Identity Security capabilities at the moment when identity became the central attack surface for enterprise AI. The Chronosphere deal extended the portfolio into observability. Together these acquisitions pushed the longer-term NGS ARR target to $20 billion by FY 2030, which implies a five-year compound annual growth rate near 29%.

→Again, 29% compound annual growth rate (we have studied the relevance of growth). Platformization momentum is holding in the underlying metrics. The company added roughly 110 net new platformizations in Q2 to reach a total above 1,550, and XSIAM crossed $500 million in ARR with more than 600 customers each paying on average close to $1 million. Non-GAAP operating margin reached 30.3 percent, the third consecutive quarter above 30 percent, and Remaining Performance Obligations grew 23 percent to $16.0 billion.

KEY RISK

Chinese authorities notified domestic firms earlier this year to halt use of cybersecurity software from select U.S. and Israeli vendors, including Palo Alto Networks. Direct China exposure is estimated in the low single digits of revenue, but the broader message matters. Geopolitical pressure is lengthening approval cycles across several international regions, and CyberArk and Chronosphere integration will weigh on near-term free cash flow margins, with FY 2026 FCF margin trimmed to 37 percent, before the platform benefits compound toward the 40 percent target by FY 2028.

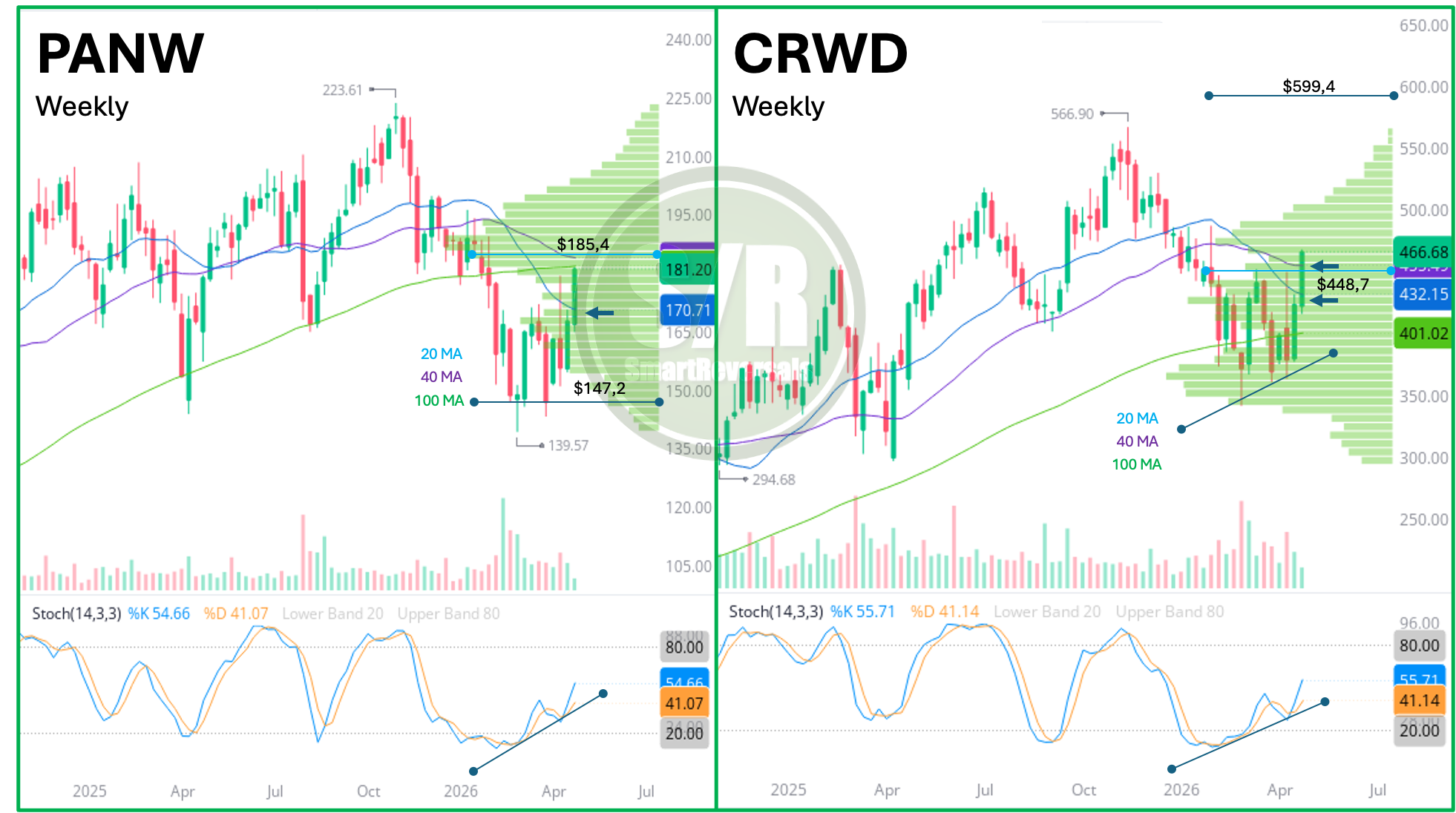

We are moving forward with the chart analysis and price targets for PANW, CRWD, PLTR, ORCL, NOW, SAP, ADBE, alongside individual deep dives for each company and the stock market update featuring tomorrow’s daily levels.

TECHNICAL ANALYSIS AND PRICE TARGETS: